How much you really need to earn to pay down your student debt

Leave it in the comments section at the bottom of this article.

Graduates need to earn £66,000 a year – considerably higher than the average UK salary – before they clear more than the interest they accrue on their student loans, according to the Institue for Fiscal Studies.

Anyone earning less than this per year will not clear any of their actual debt and will simply be paying off interest payments while their overall debt increases.

Many people describe student loans as a ‘graduate tax’, paid by graduates out of their salary until their debt is eventually wiped. But this ‘tax’ for most people is interest accumulating on their loan, meaning they never actually pay their debt down.

This means many people on middle incomes can find themselves paying hundreds of pounds her month for decades until their loan is cleared, often after 25 years or more.

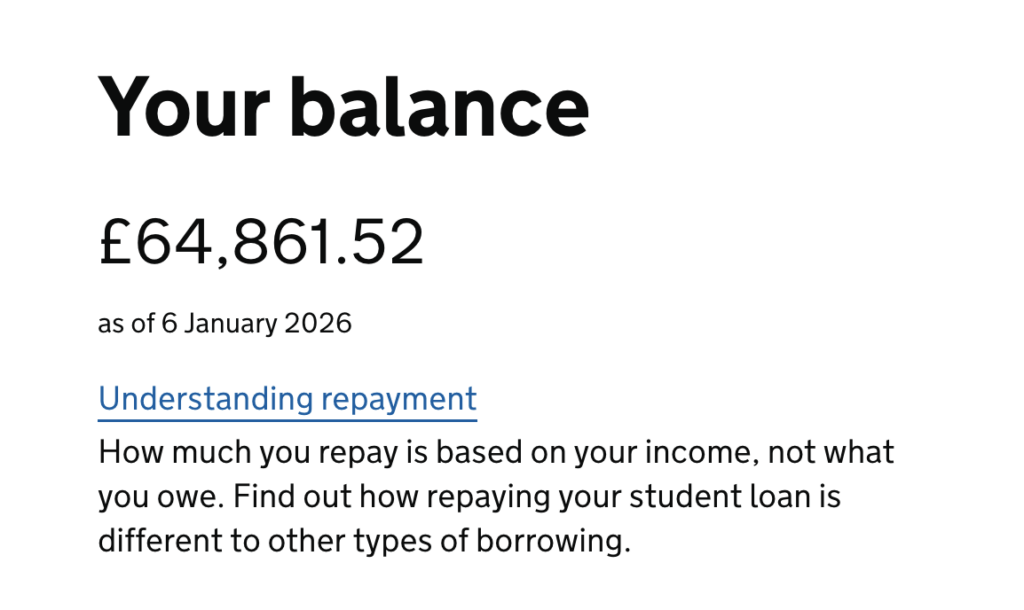

Laura Purkess, personal finance writer at Investing Insiders, still owes almost £65,000 of student debt – £10,000 more than she initially borrowed – almost a decade after graduating, despite earning well above the average salary.

For many graduates, the amount they pay off in a year is barely half of the interest added onto their debt.

Those worst off are graduates on ‘Plan 2’ loans, borrowed by those who started their degree between September 2012 and July 2023.

According to analysis by The Times, a graduate on £66,000 makes £3,295 in repayments — 9% of their earnings above the repayment threshold – but after the interest accrued (£3,286) they are paying off just £9.

Earning £66,000 or above per year would put you in the top 10% of earners in the UK, meaning 90% of earners would not be able to pay down this level of student debt.

Read our column in The Times on which degrees offer the best return on investment.

What to do if you’re struggling with student debt

First, accept what UK student loans actually are.

They behave more like a graduate tax than a normal debt. Repayments are income-based, not balance-based

You never face bailiffs or credit damage, and any remaining balance is written off after a set number of years.

The interest rate matters mainly if you are likely to fully repay.

That last point is everything.

When paying it off early can make sense

Early repayment can be rational if all of these are true:

– You are a high earner or expect to be soon

– You are on Plan 2 or Plan 5 with high interest

– You are very likely to repay the full loan before write-off

– You already have an emergency fund and no expensive consumer debt

In this case, overpaying can give you a guaranteed, risk-free return equal to the loan interest rate. That can be 6% to 7% plus, which is hard to beat after tax.

This is why some people earning £80k to £100k plus choose to clear the balance aggressively.

When early repayment is usually a mistake

For many people, overpaying is financially inefficient.

If any of the below apply, pause before paying extra:

– Your income is low to middle and not rising sharply

– You are unlikely to clear the loan before write-off

– You have no meaningful savings or investments

– You are choosing between overpaying the loan or building long-term wealth

In this scenario, extra payments often just replace money that would have been written off anyway. You give up cash today without reducing your total lifetime repayments.

Where investing fits in

Investing is not about “beating” the student loan psychologically. It is about opportunity cost.

For people unlikely to fully repay:

– Student loan repayments are capped by income

– Investing builds assets you actually own

– Over decades, long-term investing can compound far more than the loan costs

That said, investing only makes sense if:

– You are investing for the long term

– You accept market ups and downs

– You are not using money you might need soon

This is not about gambling your loan away – it’s about recognising that student loans do not behave like credit cards or mortgages.

A simple decision framework

Ask yourself three questions.

Am I likely to fully repay this loan before it is written off?

If yes, early repayment may be sensible.

If no, stop treating it like normal debt.

Is my cash better used elsewhere right now?

Emergency fund, pensions, ISAs, and a housing deposit often come first.

Would this overpayment reduce stress or just reduce flexibility?

Peace of mind matters, but flexibility has value too.

Comments

Related News

Average Subsidence Claim Soars To £20,000 Due To Heatwave – Is Your Home At Risk?

What kind of investor are you?

No comments yet. Be the first to share your thoughts!